The headlines are screaming about a "massive" win for homeowners. Mortgage rates ticked down a fraction of a percentage point, hitting a one-month low, and the media is throwing a parade. They want you to believe the "refinance boom" is back. They want you to think this is your golden ticket to "saving" money.

They are lying to you.

Or, more accurately, they are reporting on a symptom while ignoring the systemic rot. Shaving 20 basis points off a 7% loan isn't a financial victory; it’s a rounding error that the banks use to reset your 30-year clock and keep you in indentured servitude for another decade. If you’re rushing to call your broker because the 30-year fixed dropped to 6.6%, you aren't "leveraging" the market. You’re being farmed.

The Mathematical Illusion of "Savings"

The "lazy consensus" in financial journalism assumes that a lower monthly payment equals a better financial position. This is the same logic used by car salesmen to move overpriced SUVs. It ignores the Amortization Trap.

When you refinance, you aren't just changing the rate. You are resetting the schedule. Most homeowners who "jumped" on the recent rate dip are three to five years into their current loans. In those initial years, your payments are almost entirely interest. By the time you reach year five, you’ve finally started to chip away—ever so slightly—at the principal.

Refinancing back into a new 30-year loan to "save" $150 a month is a mathematical disaster. You are trading five years of equity progress for a tiny bit of monthly cash flow. You’ll end up paying tens of thousands more in total interest over the life of the new loan. The bank wins. You get a slightly cheaper monthly bill and a much later retirement date.

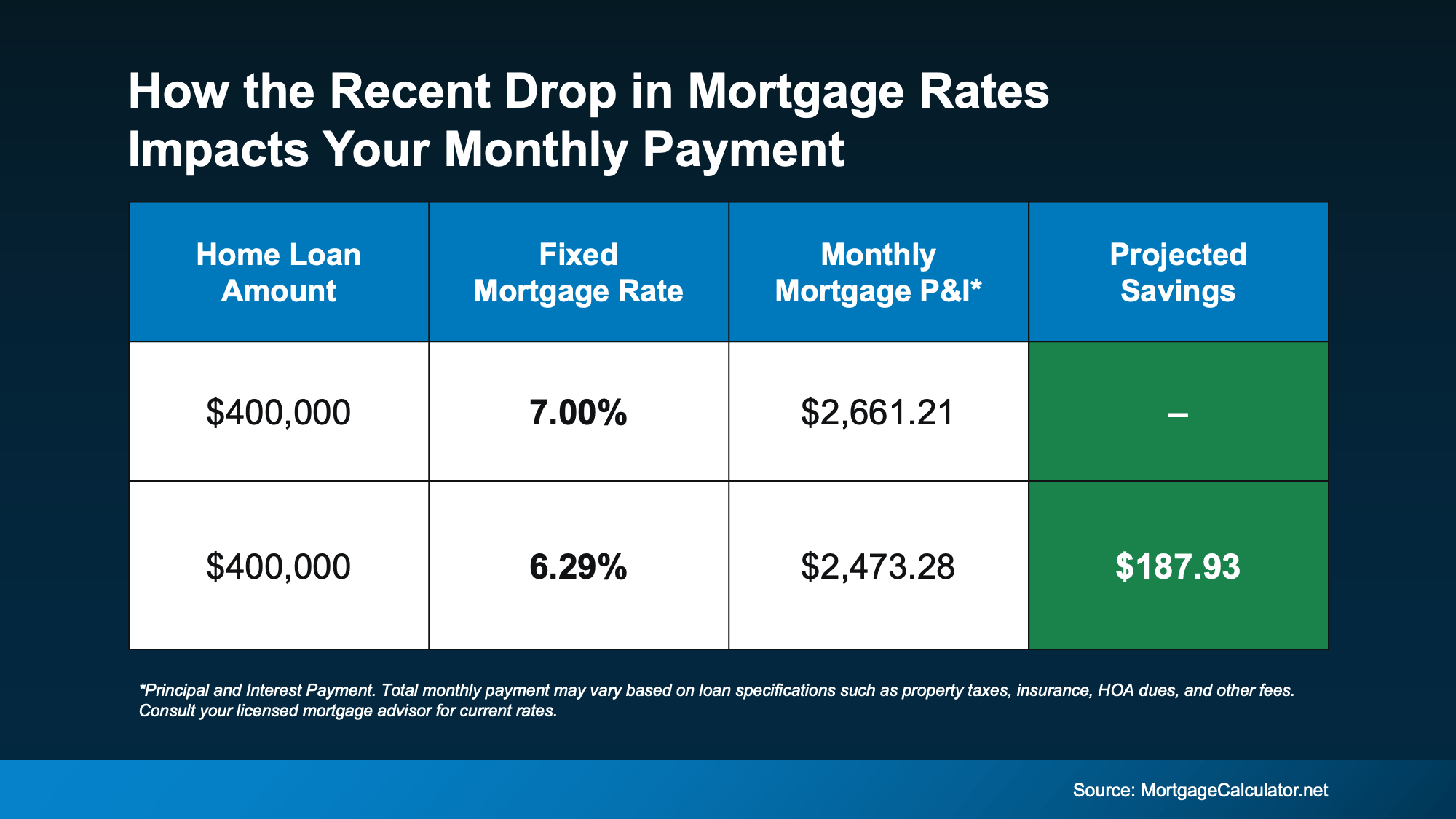

Let’s look at the actual mechanics of a standard $400,000 loan.

If you’re at 7.2% and you "dash" to refinance at 6.7%, your monthly principal and interest drops from roughly $2,715 to $2,581. A "savings" of $134. But the closing costs on that new loan will likely run you $8,000 to $12,000.

The Break-Even Reality: It will take you nearly 75 months—over six years—just to recoup the costs of the refinance. If you move or refinance again before then, you didn't save money. You wrote a donation check to the title company and the lender.

The Velocity of Capital vs. The Obsession with Rates

The obsession with "the lowest rate" is a distraction from the only metric that actually matters: The Cost of Carry.

I’ve spent fifteen years watching people obsess over whether they got a 6.5% or a 6.8% while they ignore the fact that their property taxes and insurance premiums are skyrocketing by 20% annually. The mortgage rate is the only fixed variable in a sea of volatile housing costs.

The industry insiders—the guys actually making the money—don't care about the 30-year fixed rate because they don't plan on holding the debt for 30 years. They care about the spread.

When the media reports a "surge in refinance demand," they are describing a herd of sheep running toward a cliff. These are people who are desperate for $100 in extra monthly cash because they are over-leveraged in every other aspect of their lives. They aren't refinancing to build wealth; they are refinancing to survive inflation. That isn't a "market recovery." It’s a distress signal.

Why "Wait and See" is a Loser’s Game

A common question in the "People Also Ask" sections of the web is: "Should I wait for rates to hit 5% before I buy or refinance?"

This question is fundamentally flawed. It assumes that house prices will stay stagnant while rates drop. In the real world, the relationship is inverse and aggressive. The moment rates hit a psychological floor—like 5.5%—the pent-up demand will trigger a bidding war that makes 2021 look like a library.

If you wait for a 1% drop in rates but the price of the home you want increases by 10%, you have lost. You’ll be financing a larger principal at a lower rate, but your total debt obligation is higher, and your down payment covers less ground.

Stop asking if rates are low enough. Start asking if the asset price is decoupled from reality. Right now, we are seeing a weird plateau where rates are high and prices are staying high because of a total lack of inventory. A slight dip in rates doesn't fix this; it just adds more buyers to a room with no chairs.

The Hidden Danger of the "Cash-Out" Refinance

The competitor article mentions that refinance demand is up. What they won't tell you is how much of that is "Cash-Out."

Americans are currently sitting on record levels of credit card debt. I have seen countless families "save" their finances by rolling $50,000 of 24% APR credit card debt into a new 7% mortgage. On paper, their monthly outgoings drop significantly.

In practice, they have just turned unsecured debt (which can be wiped in bankruptcy) into secured debt (which costs them their home). They have traded a short-term fire for a long-term rot. Within two years, most of these households have run the credit cards back up because they never fixed the underlying spending habit. Now they have the maxed-out cards and a bigger mortgage.

If you are refinancing to "consolidate," you aren't winning. You are liquidating your home's future value to pay for past consumption.

The Professional’s Playbook: How to Actually Win

If you actually want to beat the banks at their own game during these "rate dips," you have to stop thinking like a consumer and start thinking like a treasurer.

- The 15-Year Pivot: If rates drop, do not refinance into another 30-year. Pivot to a 15-year. The rate will be even lower, and you will actually build equity at a rate that allows for real wealth accumulation.

- The No-Cost Myth: There is no such thing as a "no-cost" refinance. You either pay the fees upfront, or they are baked into a higher interest rate. Always ask for the "Par Rate" vs. the "Discount Point" rate. If you can’t explain the difference, stay away from the closing table.

- The Principal Injection: Instead of refinancing to save $150 a month, keep your current "high" rate and simply pay an extra $150 toward your principal every month. You’ll shave years off your loan without paying $10,000 in bank fees.

The system is designed to keep you in a cycle of perpetual debt. Every time the Fed sneezes and rates drop 0.25%, the marketing machines spin up to convince you that "now is the time."

It’s the time for the banks to collect fees. It’s the time for the brokers to hit their quarterly targets. It’s rarely the time for you to actually move the needle on your net worth.

Stop celebrating the crumbs the Fed drops on the floor. A 6.7% mortgage on an overpriced house is still a liability, not an achievement. The real "refinance boom" is just a massive transfer of wealth from your future self to the financial institutions that own your front door.

If you want to be rich, stop acting like the "demand" the news is so excited about. The crowd is almost always wrong, and in the mortgage market, the crowd is currently sprinting into a hall of mirrors.

Check your ego, check your amortization schedule, and realize that the cheapest mortgage is the one you pay off the fastest, not the one with the trendiest interest rate.