You open your pay stub and there it is. That annoying gap between what you earned and what actually hit your bank account. Most of us just glance at the "Net Pay" and sigh, but if you’re trying to plan a budget or avoid a massive bill in April, you’ve probably gone looking for a federal income tax withheld chart.

It sounds simple. You look at a table, find your salary, and see a number. Right?

Actually, it's a mess.

The IRS doesn't just use one "chart" anymore. Ever since the Tax Cuts and Jobs Act (TCJA) and the subsequent redesign of Form W-4 in 2020, the way your boss takes money out of your check has become a weirdly complex calculation involving "percentage methods" and "wage bracket tables." Honestly, if you're looking for a single piece of paper that tells you exactly what to expect, you're going to be disappointed because the "chart" changes based on whether you get paid weekly, bi-weekly, or monthly.

The IRS Publication 15-T: The Real Source of Truth

If you want to see the actual math the government uses, you have to dig into IRS Publication 15-T. This is the Federal Income Tax Withholding Methods document. It’s not exactly a beach read.

Employers use this to figure out how much to skim off the top. The most common tool within this publication is the Wage Bracket Method. It’s basically a massive grid. You find your filing status—Single, Married Filing Jointly, or Head of Household—and then slide your finger down to your wage range.

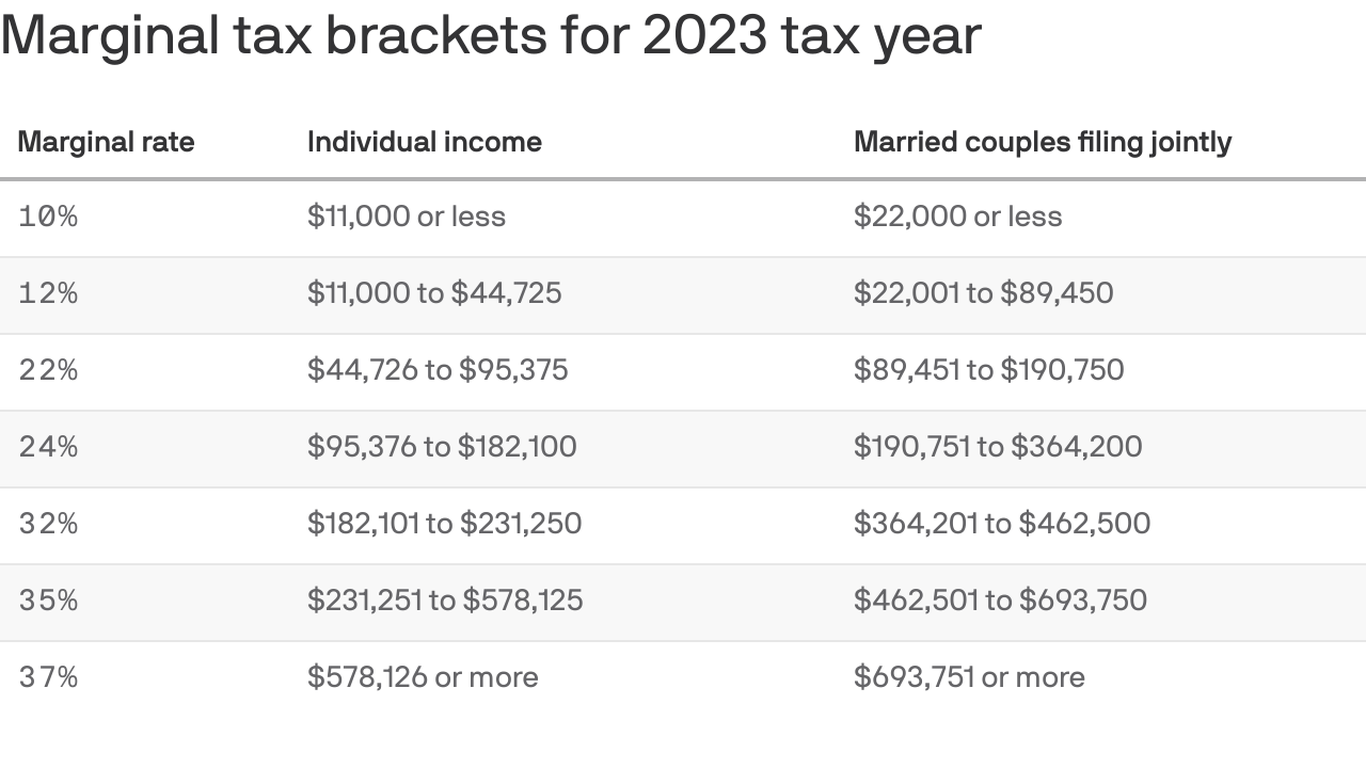

But here is the kicker: the 2025 and 2026 tax years have adjusted these brackets for inflation. If you’re looking at a federal income tax withheld chart from 2023, you’re already doing it wrong. The IRS nudges the brackets upward almost every year to prevent "bracket creep," which is when inflation pushes you into a higher tax percentage even though your standard of living hasn't actually improved.

Why your "Chart" might be lying to you

Calculators are great, but they often ignore the nuances of the 2020 W-4 redesign.

Back in the day, we had "exemptions." You’d put "1" or "2" on your form and call it a day. Those are gone. Dead. Buried. Now, the withholding tables rely on a much more invasive set of questions. Do you have a side hustle? Does your spouse work? Do you claim the Child Tax Credit?

If you haven't updated your W-4 in four years, your employer is likely using a "legacy" calculation that might be significantly over-withholding or under-withholding your cash. This is why some people get a $5,000 refund (which is basically just a 0% interest loan to the government) while others get hit with a "failure to pay" penalty.

How the Wage Bracket Tables Actually Work

Let’s look at how a standard federal income tax withheld chart functions for someone getting paid bi-weekly in 2026.

If you are Single and earn roughly $2,000 every two weeks, the IRS doesn't just tax that whole $2,000. First, the "chart" subtracts a standard deduction amount. For a single filer in 2026, that's a significant chunk of change. Only the money above that threshold is subject to the tiered percentages—10%, 12%, 22%, and so on.

The 12% bracket is the "sweet spot" where most Americans live. If you’re a single filer making between roughly $11,925 and $48,475 (taxable income), you’re in that 12% zone. But wait. That doesn't mean you pay 12% on everything. You pay 10% on the first bucket of money and 12% on the rest.

The federal income tax withheld chart is designed to automate this "bucket" logic so your HR software doesn't have to be a math genius.

The "Step 2" Trap

The biggest mistake people make when looking at withholding charts is ignoring "Step 2" of the W-4. This is for households with two jobs. If you and your spouse both work and you both check "Single" or "Married Filing Jointly" without checking the "Multiple Jobs" box, the withholding tables assume you are the only breadwinner.

Result? The system gives you two standard deductions.

The IRS thinks you have more "tax-free" income than you actually do. Come April, the IRS realizes you "double-dipped" on the deduction, and suddenly you owe $3,000. It’s a gut punch. Using a federal income tax withheld chart without accounting for a second income is like trying to navigate a forest with half a map.

The Percentage Method vs. The Wage Bracket Method

Employers usually choose between two ways to read the "chart."

- The Wage Bracket Method: This is the literal table. It’s limited to people making under about $100k a year (depending on pay frequency). It’s "step-wise," meaning it moves in $10 or $25 increments.

- The Percentage Method: This is for the high earners or the automated payroll systems like ADP or Gusto. It’s more precise. It uses a mathematical formula to find the exact penny to withhold.

If you’re a freelancer or a "1099" worker, none of this happens automatically. You are the payroll department. You should be looking at these charts to figure out your quarterly estimated payments. If you wait until the end of the year to pay, the IRS will slap you with an underpayment penalty that feels like a very expensive parking ticket you can't fight.

Credits Change Everything

Let’s talk about the Child Tax Credit (CTC).

If you have two kids under 17, you’re looking at a $4,000 credit (subject to phase-outs and legislation changes). On the W-4, you account for this in Step 3. This actually reduces the amount of federal tax withheld.

If you use a generic federal income tax withheld chart online and it says they should take out $400, but you have kids, your actual withholding might be $250. This isn't a mistake. It's the system working as intended to put more money in your pocket during the year rather than making you wait for a refund check.

Real-World Nuance: The "Bonus" Problem

Ever notice that your bonus check feels tiny?

People often think their bonus "pushed them into a higher bracket." That’s a myth. Well, mostly.

What actually happens is that the federal income tax withheld chart sees a $5,000 bonus check on a Friday and assumes you make $5,000 every Friday. It thinks you make $260,000 a year. So, the software withholdings taxes at the 32% or 35% rate.

Alternatively, many employers use the "supplemental rate," which is a flat 22%. If you’re normally in the 12% bracket, that 22% feels like a robbery. But don't worry—you get that over-payment back when you file your taxes. It’s annoying, but it’s not lost money.

Actionable Steps to Get Your Withholding Right

Stop guessing. If you want to master your paycheck, do these three things right now:

- Run the IRS Withholding Estimator: Forget the static PDF charts for a second. Go to the IRS website and use their "Tax Withholding Estimator" tool. You’ll need your last pay stub and your spouse's stub. It is the most accurate way to see if your current withholding matches your year-end liability.

- Adjust for Life Events: Did you get married? Have a baby? Buy a house? These aren't just Facebook updates; they are tax triggers. Any time your life changes, you should submit a new W-4.

- Check the "Extra Withholding" Box: If you have a side gig or significant interest income, you can tell your employer to take out an extra $50 or $100 per check in Step 4(c). This is the "peace of mind" button. It ensures you won't be scrambling for cash in April.

The federal income tax withheld chart is a tool, not a rule. It’s a baseline for how the government expects to be paid. By understanding that these charts rely on the information you provide on your W-4, you take control of your cash flow. If you want more money in your monthly paycheck, you adjust the credits. If you want a big "forced savings" check in the spring, you do the opposite. Just don't let the "chart" surprise you.

For those who really want to see the raw data, download the latest version of IRS Publication 15-T. It contains the worksheets that explain how to transition from a gross wage to a net withholding amount, accounting for the standard deduction and the specific tax rates for the current year. It’s the ultimate guide for anyone who wants to verify that their HR department isn't making a clerical error.

Check your next pay stub. If the federal tax withheld seems wildly off compared to the 2026 brackets, it’s time to have a chat with your payroll manager or your tax pro. Usually, it's just a simple W-4 update away from being fixed.

Next Steps for Accuracy

- Download your 3 most recent pay stubs. Look at the "Federal Tax" line.

- Compare that amount to the "Percentage Method" tables in Pub 15-T for your specific pay frequency (Weekly vs. Bi-weekly).

- Calculate your projected total tax for the year by multiplying your current withholding by the remaining pay periods.

- Submit a revised W-4 if your projected withholding is more than 10% higher or lower than your estimated tax bill.